The comcast business split marks a historic pivot point that effectively dismantles the era of the all-encompassing media conglomerate. When a massive player like Comcast decides to carve out its prized NBCUniversal and Sky assets from its connectivity bedrock, it is not merely a corporate reshuffling; it is a profound admission that the old ‘pipe-and-content’ synergy model no longer holds the weight it once did. I have followed the telecommunications sector for over fifteen years, and witnessing a giant of this magnitude acknowledge that its internal structure has reached a mathematical ceiling is a rare look into the friction inherent in modern corporate evolution. By separating the high-growth, high-risk world of global entertainment from the essential, utility-like nature of broadband and wireless, the company is preparing for a new reality where specialization, rather than raw scale, defines success.

Quick Summary

The Comcast business split formally separates NBCUniversal and Sky from the legacy broadband and wireless connectivity infrastructure.

This restructuring aims to eliminate the ‘conglomerate discount’ that has suppressed the share price for several years.

Two distinct entities will emerge: a content-focused media powerhouse and a connectivity-focused technology utility.

Michael Angelakis will lead the new standalone Comcast connectivity business, while Mike Cavanagh will head the NBCUniversal/Sky entertainment entity.

The process is expected to be finalized by mid-2027, with Comcast retaining a 19.9% stake in the media spin-off for a one-year transition period.

The Direct Answer: Why Is This Happening?

If you are wondering what this means for your involvement as an investor, customer, or employee, the direct answer is that Comcast is betting on agility over bulk. For over a decade, the logic was simple: own the wires and the content flowing through them, and you control the ecosystem. However, that synergy was largely eroded by the rise of streaming platforms that bypass traditional cable bundles entirely. The split is designed to allow each business to pursue the capital structure and investment strategy that matches its specific reality. The media side needs creative risk-taking and global scalability, while the broadband side needs a laser focus on infrastructure efficiency and operational stability. By separating them, the market can finally value each entity based on its own merits rather than grouping them into a distorted, single-entity balance sheet.

The Strategic Logic Behind the Decoupling

When I first analyzed the announcement, I was immediately struck by the sheer scale of the shift. For years, the cable segment acted as a massive cash cow, subsidizing the volatility of film studios and the heavy operational costs of international pay-TV platforms like Sky. In my experience observing these types of corporate maneuvers, this setup works only when the markets are growing in tandem. When the landscape fractures—as it has with the massive decline of linear television—the combination becomes a liability.

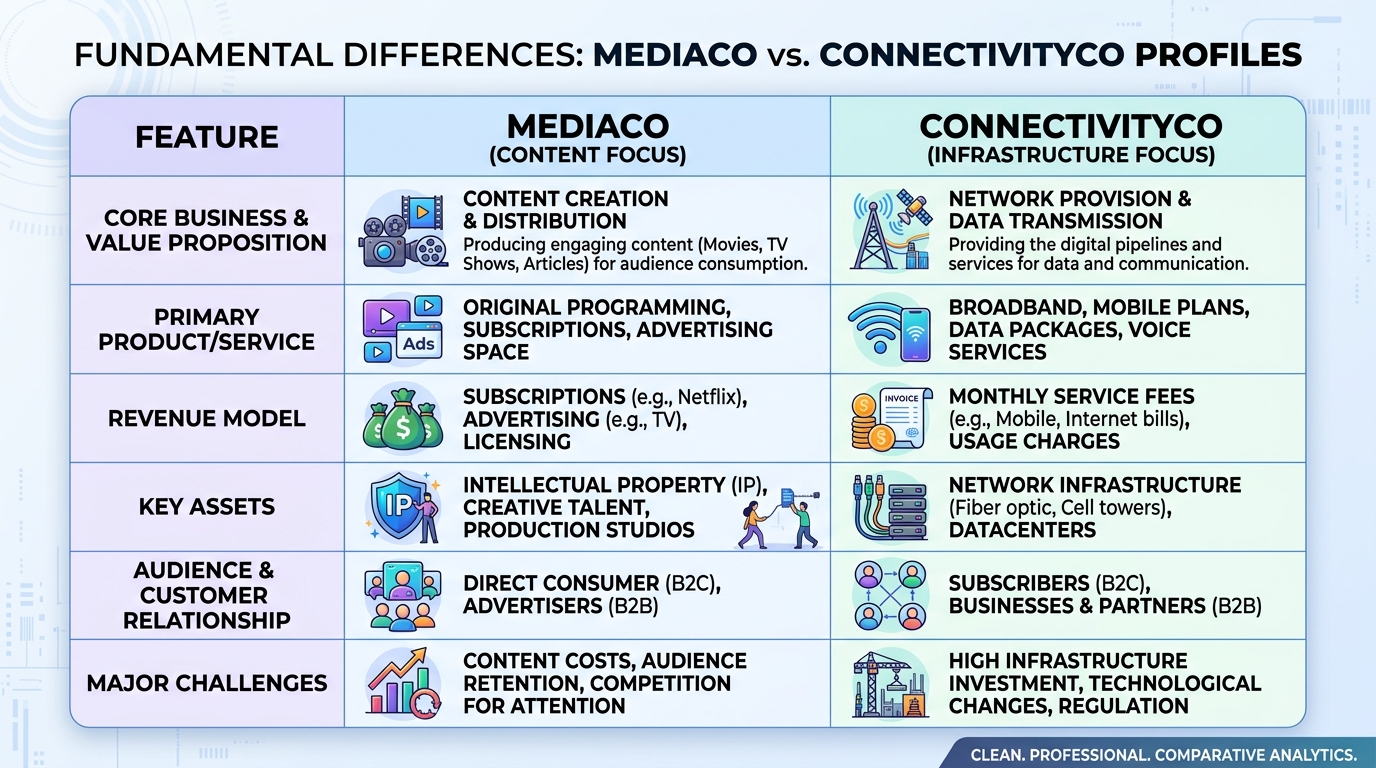

Broadband providers, or ‘CableCo,’ are essentially modern utilities. Their success depends on network reliability, capital expenditure (CapEx) control, and keeping churn rates to a minimum as they face competition from fiber-to-the-home and satellite internet providers. Media companies, or ‘MediaCo,’ thrive on an entirely different set of metrics: blockbuster film releases, theme park performance, and the sheer subscriber volume of streaming platforms like Peacock. Forcing a single board of directors to balance these two conflicting missions resulted in a strategic incoherence that the market grew tired of seeing.

Analyzing the Two New Entities

The Connectivity Powerhouse (The New Comcast)

The broadband-focused entity will operate under the Xfinity brand and prioritize the ‘last mile’ of internet and mobile connectivity. This business model is built on stability and dividend potential. By shedding the volatile entertainment assets, the management team, headed by former CFO Michael Angelakis, can focus entirely on defending its market share against regional fiber competitors and optimizing the profitability of its existing network footprint.

I believe this entity will behave much more like a regulated utility than a media firm. It will be under intense pressure to maintain high margins while keeping capital expenditure at sustainable levels. Investors looking for a predictable, steady stream of cash flow will likely find this the more attractive side of the split, provided they are not looking for the explosive growth that usually accompanies tech-heavy media plays.

The Entertainment Powerhouse (MediaCo)

This entity will house NBCUniversal, the Universal film and television studios, the theme parks, and the international giant Sky. Led by current co-CEO Mike Cavanagh, this unit has a clear, albeit difficult, mission: win the streaming wars. Without the anchor of the cable business, this entity is now a pure-play content company. It will need to act with extreme speed to scale its streaming service, Peacock, to compete with the likes of Netflix and Disney.

One thing that is often misunderstood is the role of theme parks in this equation. Many analysts overlook the cash-generating power of the Universal parks, which provide a physical-world hedge against the digital volatility of streaming. This media entity is now a more transparent target for potential future M&A, as regulatory hurdles are generally lower for standalone media companies than they are for telecommunications monopolies. I expect the leadership here to be far more aggressive with their intellectual property development and international expansion.

The M&A Ripple Effect and Future Consolidation

One of the most frequent points of debate is whether this split is just the first step toward a sale. While Brian Roberts has been vocal in stating that this is ‘absolutely not’ the case, I have seen enough of these corporate restructurings to be slightly skeptical. When you simplify a balance sheet, you inherently make the company a more attractive snack for larger tech conglomerates.

Companies like Apple or even private equity players are arguably more likely to look at a standalone NBCUniversal than they were when it was tethered to a debt-heavy regional telecom provider. On the flip side, the connectivity side is likely to seek its own form of horizontal consolidation. Do not be surprised if we see the new Comcast connectivity arm look to merge with other regional players to form a more unified, national backbone for internet distribution. This would be a strategic move to gain better negotiating leverage with other content providers.

Who Should Consider the Post-Split Strategy

Choosing which side of the split to favor depends entirely on your investment philosophy. This decision is not a one-size-fits-all situation; it is a choice between two distinct business models that will now trade on their own unique characteristics.

This Is Ideal For…

Growth-Oriented Investors: If you favor the high-margin, high-risk world of intellectual property, gaming, and streaming, the new media entity is your target. You are effectively buying into a ‘content machine’ that is now free to pursue global growth without the baggage of a legacy cable business.

Dividend-Focused Investors: The new connectivity-focused Comcast will be the home for those who prioritize stability and predictable revenue. This is a classic utility play that offers a defensive position against market volatility.

You Might Want to Skip This If…

You Prefer Pure-Play Tech: If you are looking for software-driven growth companies, neither of these might fit. The media side is still burdened by the legacy costs of linear TV, and the connectivity side is essentially a capital-intensive infrastructure business.

- You Have a Low Risk Appetite: The media side of this split will be volatile. If you cannot stomach the fluctuations associated with film production cycles, streaming subscriber churn, and theme park attendance, this entity is not for you.

- fortune.com

- www.wral.com

- www.businessinsider.com

- variety.com

- www.nbcnews.com

- es.tradingview.com

- intellectia.ai

Cost and Valuation Dynamics

| Feature | ConnectivityCo (Broadband) | MediaCo (Entertainment) |

|---|---|---|

| Core Focus | Network Infrastructure & ISP | Content Production & Streaming |

| Revenue Profile | Stable, subscription-based | Volatile, IP-driven/Box Office |

| Competitive Hurdle | Fiber expansion & Satellite | Global streaming giants (Netflix) |

| Key Capital Driver | Infrastructure Maintenance | Content Creation (R&D) |

The market’s reaction—an immediate jump in stock price—validates the idea that investors were penalizing Comcast for its ‘conglomerate discount.’ By separating, the company is effectively removing the administrative bloat and the strategic confusion that often accompanies multi-divisional empires. While the transaction itself involves significant legal and accounting costs, these are non-recurring expenses. The potential for a ‘re-rating’ of the shares, where the market assigns a higher multiple to the individual parts than it did to the whole, is the primary economic driver behind this move.

Common Mistakes to Avoid

1. Assuming the ‘Bundle’ is Still the Future

Many retail investors make the mistake of mourning the loss of the ‘synergy’ of the traditional bundle. They fear that losing the ability to sell internet and TV in one package will destroy value. In reality, the bundle was already dying. I have seen households cut the cord at an alarming rate over the last five years, rendering that cross-selling advantage largely theoretical. Expecting the bundle to be the savior of the industry is to ignore the actual shift in how consumers interact with content.

2. Ignoring the Regulatory Landscape

Another major misconception is that this move is purely about internal financial optimization. It is also a sophisticated defensive move against antitrust pressure. By separating the ‘pipes’ from the ‘content,’ the new entities create a firewall against regulators who worry about vertical integration. If you are analyzing this move, you must account for the fact that this split significantly lowers the political and regulatory temperature surrounding these two businesses.

Frequently Asked Questions

Does the Comcast business split affect my monthly internet bill?

In the short term, you should not see any dramatic changes to your bill. The split is primarily a corporate and balance-sheet restructuring. Your service, network reliability, and customer support will continue under the Xfinity brand as before. However, over the long term, the pressure for the standalone connectivity business to maintain higher profit margins could lead to changes in pricing models or data usage policies as it attempts to maximize revenue without the backing of the entertainment unit.

Why did it take so long for this to happen?

Fifteen years ago, the logic of vertical integration was the gold standard. The rise of streaming and the total disruption of linear TV took time to reach a tipping point. When Comcast acquired NBCUniversal, content providers were genuinely afraid of losing their distribution channels. The explosion of SVOD (Subscription Video on Demand) and the rapid decline of cable television were the final factors that turned the old ‘all-under-one-roof’ structure from an advantage into a massive liability.

Is the new media entity going to be acquired by a tech giant?

While market theory loves to speculate, I advise caution here. Companies like Netflix have shown little interest in acquiring traditional studio infrastructure; they prefer to build their own intellectual property. However, companies like Apple, which have been searching for a stronger content library to anchor their ecosystem, might find a standalone NBCUniversal very tempting. The primary hurdle will always be the regulatory environment, which remains very strict on large-scale media consolidations.

Conclusion: The Road Ahead

The Comcast business split represents the definitive acknowledgement that the media industry is no longer about scale, but about specialization. By separating the capital-intensive utility of broadband from the creative volatility of global media, Comcast is preparing for a future where agility is the only real competitive advantage. My personal recommendation for any stakeholder is to watch the debt allocation during this transition closely. The entity that begins its new life with a cleaner, more manageable balance sheet will be the one best positioned to dominate its respective sector in the coming decade.

As we look forward to the mid-2027 completion date, the most important metric to track is not the headline growth of one entity or the other, but the efficiency with which they shed their previous organizational bloat. This is a story of unwinding a decade-long experiment, and for investors and industry followers, it offers a clean slate to re-evaluate where the true value lies. The conglomerate veil has been lifted, and the result is a clearer look at two distinct, and potentially more valuable, business models.