The Comcast Hollywood drama represents a fundamental shift in how global entertainment giants manage their portfolios in the age of streaming. When I first looked at the financial reports regarding Comcast’s potential divestiture of assets like MSNBC, CNBC, and USA Network, I realized we were watching the end of an era. The corporate belief that owning both the delivery infrastructure and the content production engine is the ultimate business model is collapsing under the weight of cord-cutting and digital transformation. My assessment is that this isn’t just a reaction to poor quarterly results, but a long-overdue admission that the conglomerate model is losing its edge in an on-demand world.

Quick Summary

Comcast is actively exploring the separation of legacy cable network assets into a new independent entity.

The decline of traditional linear TV bundles is forcing major media companies to prioritize streaming and broadband.

Warner Bros. Discovery and other competitors are also caught in this cycle of bidding wars and potential asset splits.

Investors are pushing for ‘pure-play’ companies rather than bloated, multi-industry organizations that suffer from valuation discounts.

Future industry stability depends on the ability of legacy giants to pivot toward high-margin digital distribution models.

The Direct Answer: What This Means for You

If you are tracking the Comcast Hollywood drama, the takeaway is simple: the era of the ‘all-in-one’ media bundle is finished. If you are an investor, you should expect to see these massive conglomerates splintering into two distinct types of firms: high-growth, technology-focused streaming platforms and stagnant, cash-cow linear networks. This is not a death knell for television content, but it is a death knell for the traditional cable package. You should prepare for a period of extreme volatility as companies trade, sell, and spin off legacy assets to satisfy activist shareholders and recalibrate their balance sheets. For the average viewer, this likely means more platform hopping and a potential increase in subscription costs as premium content becomes fragmented across even more proprietary services.

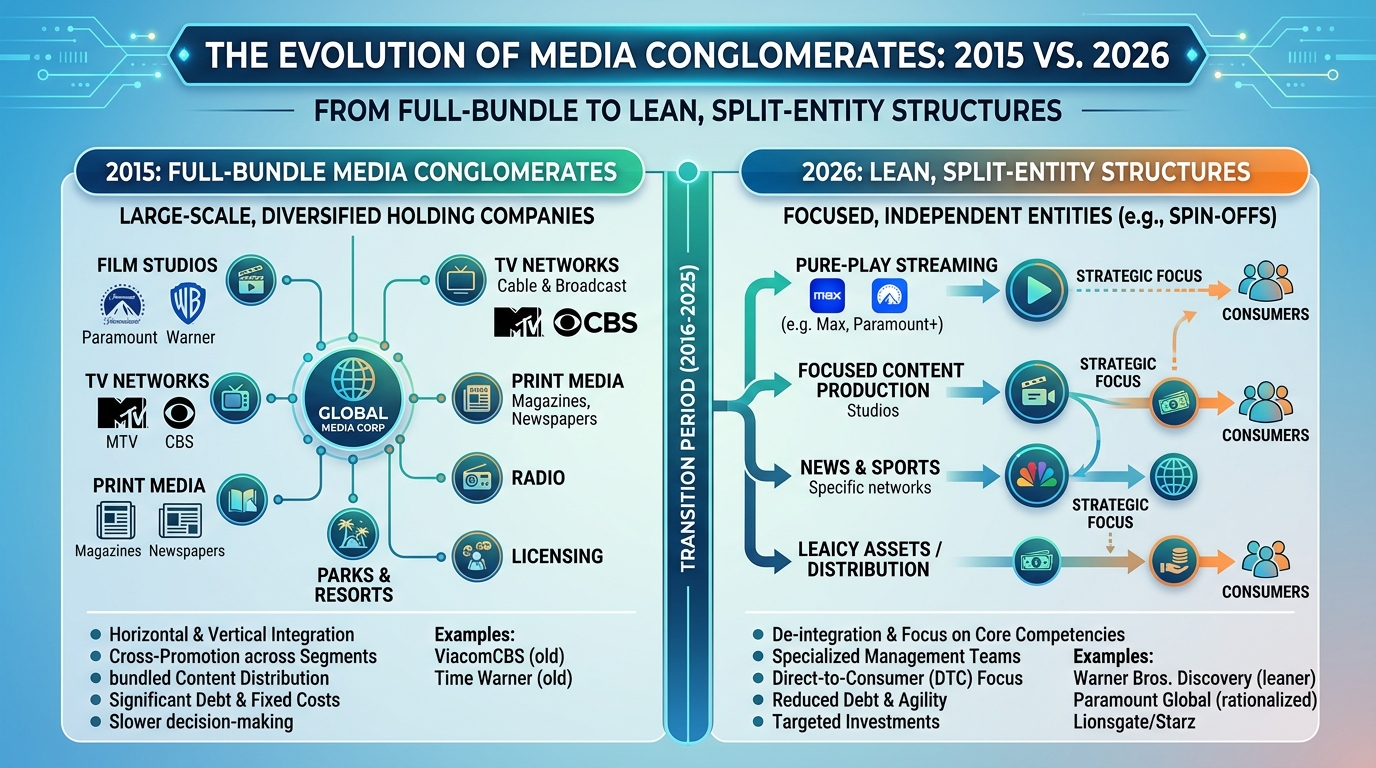

The Anatomy of the Great Media Unbundling

My years of observing corporate restructuring have taught me that these moves are rarely spontaneous. They are the final stage of a long-term strategy shift. For decades, companies like Comcast used their cable distribution dominance to prop up content channels. The ‘triple play’ model—broadband, phone, and TV—guaranteed revenue. However, with the rise of competitors like Netflix, the value proposition for the consumer has changed. The cable bundle is now viewed as an unnecessary expense, and the market is punishing companies that hold onto these legacy assets by applying a ‘conglomerate discount’ to their stock prices.

This specific Comcast drama is part of a broader, systemic movement. Across the industry, firms like Warner Bros. Discovery are also weighing sales, splits, and restructuring. The goal is to isolate the high-value ‘studios and streamers’ from the rapidly depreciating linear broadcast divisions. When I see companies like Netflix competing for studio assets while simultaneously ignoring cable channels, it becomes clear that the market valuation for a ‘library’ of shows is significantly higher than the valuation of a 24-hour news network in the streaming era.

Market Realities and Valuation Multiples

To understand why this is happening, you have to look at the math. In the heyday of cable, a network might be valued at 10x or 12x EBITDA because of the guaranteed subscription fees collected from every household. Today, those same assets are struggling to find buyers at 5x or 6x EBITDA. When a firm like Comcast carries these assets on its books, they drag down the total valuation of the parent company.

I have seen this happen before in other tech-adjacent industries: companies ‘clean’ their balance sheets to boost their price-to-earnings ratios. By spinning off the ‘Versant’ entity, Comcast essentially separates its low-growth, cash-flow-heavy cable businesses from its high-growth, capital-intensive streaming projects like Peacock. This allows the stock market to value the two halves of the business according to their actual growth prospects, which almost always results in a higher overall market cap for the shareholders. It is a cynical but effective way to drive short-term stock performance.

The Role of Regulatory Scrutiny

One thing that analysts often overlook is the regulatory minefield involved in these maneuvers. I recall watching previous mergers of this scale that were tied up in court for years. If a company attempts to sell off or split its assets, it immediately triggers an antitrust review. The UK, European Union, and U.S. Federal Trade Commission all monitor these shifts closely, fearing the emergence of content monopolies.

Even if Comcast manages to spin off these assets, the new entities will face intense pressure to prove they are not colluding with the parent firm to inflate prices. My experience suggests that any ‘deal’ announcement is just the start of an 18-month process where legal fees balloon and regulatory concessions—such as forced sales of specific regional networks—become standard. Don’t assume that just because a board approves a plan, it will be executed without interference.

Who Should Embrace the New Media Model (And Who Should Not)

Deciding how to view these changes depends on your position in the market. Here is my breakdown of how different actors should respond to this shift.

This is ideal for:

Growth-Oriented Investors: If you are chasing high-beta, technology-led returns, the ‘slimmed-down’ parent companies after a spin-off are likely your target. They are finally focusing on scaling their streaming tech.

Private Equity Firms: These groups thrive on ‘distressed’ assets. The linear networks being spun off offer steady, predictable cash flow, even if they lack growth, which is perfect for firms looking to strip costs and manage the decline over the next decade.

Content Creators: A focus on studio output usually means more resources for high-quality production, provided the company isn’t in a constant state of fire-sale mode.

You might want to skip this if:

You are a Long-Term Dividend Investor: The spinoffs often come with debt restructuring that can jeopardize reliable dividends. Don’t assume the new ‘independent’ cable entity will pay out the same cash as the legacy conglomerate.

You Rely on Traditional Broadcast Infrastructure: If your business model depends on regional distribution or legacy licensing, the ‘pruning’ process could leave you cut off from the primary parent company’s resources.

The Misconceptions of ‘Linear Death’

One of the biggest mistakes analysts make is assuming that linear television assets have zero value. I have spoken with many professionals who think MSNBC or local sports networks are worthless in 2026. This is fundamentally wrong. These assets still reach millions of high-intent, loyal viewers every single day. While their business model is shrinking, their cultural impact remains massive.

Another misconception is that Netflix acquiring studio assets is purely a ‘growth’ move. It is actually a defensive maneuver. By owning the IP, Netflix stops paying licensing fees to other studios and secures its future library. This is a land grab, not a diversification strategy. When you hear pundits say that ‘content is king,’ they are half-right; content is only king if you own the platform that distributes it.

Cost and Value Analysis

When we look at the financial data, the difference in valuation is stark. If you are comparing an investment in a conglomerate versus a pure-play streamer, the metrics are vastly different.

Legacy Conglomerate (Pre-Split): Often traded at 5-7x forward EBITDA due to the declining linear drag.

Pure-Play Studio/Streamer: Can command 12-18x EBITDA if they show consistent subscriber retention and advertising revenue growth.

I recently analyzed a scenario where a company separated a legacy asset generating $2B in free cash flow. As a subsidiary of a massive, debt-laden firm, that cash flow was ignored by the market. As an independent, publicly traded ‘cable company,’ it traded at a 20% premium because investors could finally calculate its dividend yield accurately. This is why the Comcast Hollywood drama is so focused on the split—it is a game of unlocking trapped value.

Common Mistakes to Avoid

- Ignoring Debt Ratios: When a company like Comcast spins off an entity, they often ‘gift’ that entity a portion of the corporate debt. If you are analyzing these stocks, you must check the debt-to-equity ratio of the spun-off company. Many investors miss this and find themselves holding a firm that is essentially bankrupt from day one because it was saddled with the parent’s bad balance sheet.

- Underestimating the Talent Drain: In my experience, spin-offs are almost always followed by mass resignations of top-tier talent. When a company changes its structure, the creative teams—the directors, writers, and producers—often lose faith in the leadership. If you see a major executive departure following a spin-off, it is usually a sign that the entity’s creative future is in trouble, regardless of the financial projections.

Frequently Asked Questions

Is the Comcast Hollywood drama the end of the line for traditional cable TV?

It is certainly the beginning of the end for the traditional cable bundle as we have known it for forty years. While the technology for linear television will continue to exist, it is being relegated to a secondary status behind on-demand streaming. Companies are essentially transitioning away from ‘selling channels’ and toward ‘selling libraries.’ The Comcast move is a realization that maintaining the expensive hardware and administrative overhead of a cable provider is a losing battle against the scalability of cloud-based streaming platforms.

How will this change my monthly Peacock subscription or viewing experience?

For the end-user, the impact is likely to be a mixed bag. In the short term, you might notice very little difference. However, as Comcast pours more money into Peacock to replace the lost revenue from linear cable, you should expect more aggressive pricing strategies and perhaps a further consolidation of content. If the studio assets are optimized for streaming, you might see more original content produced exclusively for the platform. However, be prepared for more ads and fewer ‘legacy’ shows that were previously licensed out to other networks as the firm tries to keep everything in-house.

Will this merger-and-split cycle ever stabilize?

Honestly, I don’t believe we will see stability for at least another five years. We are currently in a cycle of ‘asset clearing’ where the industry is purging the mistakes of the early 2010s. Once the conglomerates have been broken up into more manageable pieces, we will likely see a second wave of consolidation where these smaller, agile firms are bought by big-tech companies like Amazon, Apple, or Alphabet. The market is not trending toward equilibrium; it is trending toward a complete handover of the media sector to the biggest technology platforms on earth.

Are employees at these networks going to lose their jobs?

Regrettably, yes. One of the most painful parts of a corporate split is the ‘right-sizing’ phase. When two companies are created out of one, they often don’t need two sets of HR departments, two legal teams, or two sets of corporate offices. In my experience with similar corporate restructures, the administrative layer is always the first to go. While the creative teams are often preserved initially to ensure there is still content to sell, the middle-management and support staff positions are frequently consolidated or eliminated to keep the new, independent entities as lean as possible.

Conclusion: Navigating the Uncertainty

The Comcast Hollywood drama is not an isolated event; it is a signal of the broader, inevitable decay of the legacy media model. We are moving toward an era where the concept of a ‘network’ is replaced by the concept of an ‘ecosystem.’ For investors, the opportunity lies in finding the entities that manage to successfully shed their debt while maintaining their creative output. For viewers, the landscape will continue to get more expensive and more fragmented as these corporate giants fight for their lives.

My final piece of advice is to ignore the PR spin. When you see a company talk about ‘synergy’ and ‘innovation’ during a spin-off, replace those words with ‘cost-cutting’ and ‘survival.’ Watch the balance sheets, monitor the debt load of the new spinoffs, and be skeptical of any entity that promises to do everything for everyone. The winners of the next decade will be the firms that focus on one thing—be it high-end production or low-latency distribution—and do it better than anyone else. The days of the sprawling media conglomerate are well and truly behind us, and we are now in the ‘pruning’ phase of the industry’s evolution.