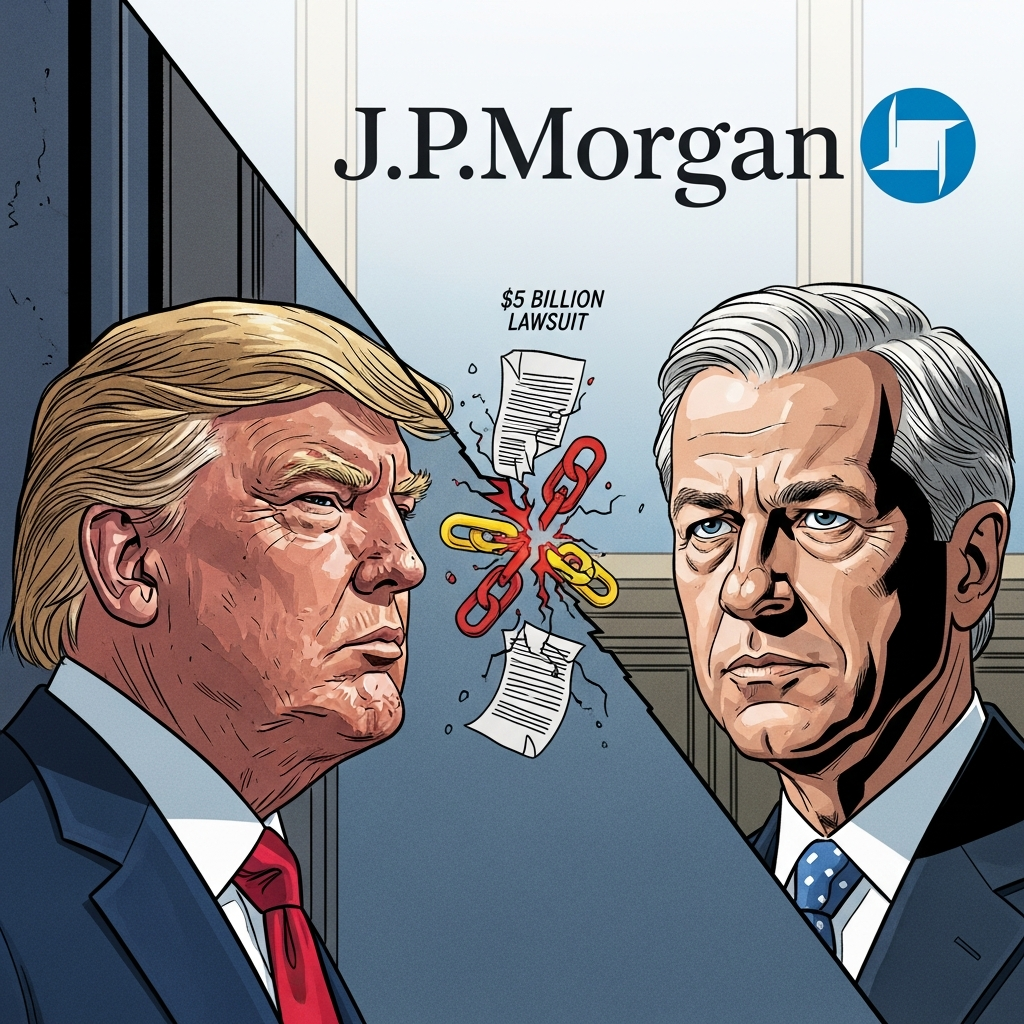

JPMorgan Chase has formally conceded a significant detail in a high-stakes legal battle: the bank closed former President Donald Trump’s accounts and those of his various businesses following the January 6, 2021, attack on the U.S. Capitol. This pivotal admission, made in a recent court filing, marks a turning point in Trump’s $5 billion “debanking” lawsuit against the financial giant and its CEO, Jamie Dimon. The revelation puts the politically charged issue of financial discrimination and “reputational risk” squarely in the spotlight, raising questions about banks’ power to sever client relationships.

The lawsuit alleges that Trump’s accounts were terminated for political reasons, causing substantial disruption to his vast business operations. This case not only pits a former president against one of the world’s largest banks but also reflects a broader national debate concerning access to financial services for individuals and entities with controversial political affiliations.

The Core Revelation: JPMorgan’s Formal Admission

For the first time in writing, JPMorgan Chase has unequivocally stated that it ended its banking relationship with Donald Trump. This significant acknowledgment emerged from a court document filed as part of Trump’s ongoing legal challenge. Prior to this, the bank had consistently avoided direct written confirmations, often citing client privacy laws and discussing account closures only in hypothetical terms.

The formal statement came from Dan Wilkening, JPMorgan’s former chief administrative officer. In the filing, Wilkening confirmed that “certain accounts maintained with JPMorgan’s CB and PB would be closed” in February 2021. CB and PB refer to the bank’s commercial banking and private banking divisions, respectively. This admission confirms the closures occurred just weeks after the Jan. 6 Capitol incident.

A Shift in Stance

Specific letters detailing the account closures were sent on February 19, 2021, to Trump and entities such as The Trump Corporation. These letters, now part of the public record, explicitly informed Trump that JPMorgan Chase was ending its banking relationship. One notable excerpt stated, “We may determine that a client’s interests are no longer served by maintaining a relationship… this letter is to respectfully inform you that we will need to end our current relationship.”

Following these notices, JPMorgan worked with Trump and his companies to facilitate the transfer of “hundreds of millions of dollars” to other financial institutions. Accounts were officially closed by April 19, 2021, adhering to the standard 60-day notice period often stipulated in banking agreements. This detailed timeline and financial handling information add crucial context to the dispute.

Trump’s $5 Billion Lawsuit: Allegations and Demands

Donald Trump’s lawsuit, initially filed in Florida state court, seeks a staggering $5 billion in damages. He accuses JPMorgan and Jamie Dimon of “debanking” him due to political motivations. The legal complaint levels serious charges, including trade libel and violations of both state and federal unfair and deceptive trade practices acts. Trump’s legal team contends that the bank’s actions were arbitrary and politically driven, causing immense financial harm.

The lawsuit further claims that Trump personally reached out to Jamie Dimon after receiving the initial notices. Dimon reportedly assured Trump that he would investigate the matter. However, the suit alleges that Dimon failed to follow up, leaving Trump without a resolution. This personal aspect adds a layer of contention to the corporate dispute.

The “Blacklist” Claim

A central and particularly damaging accusation from Trump’s lawyers is the claim that JPMorgan placed him and his companies on a reputational “blacklist.” They argue that this alleged list prevents Trump from opening new accounts with JPMorgan and potentially other financial institutions in the future. This “blacklist” has yet to be clearly defined by Trump’s legal team, prompting JPMorgan’s lawyers to indicate they will respond once more specifics are provided. Such a blacklist, if proven, could significantly impede an individual’s financial freedom.

The Debanking Debate: A Politically Charged Landscape

The core of this legal battle revolves around “debanking,” a practice where financial institutions close customer accounts or refuse to provide services like loans. While once an obscure financial term, debanking has rapidly evolved into a highly politicized issue in recent years. Conservative politicians and figures, including Trump, increasingly allege that banks are discriminating against them and their affiliated interests. These claims often cite “reputational risk” as a pretext for denying services, especially after sensitive events like the Jan. 6 Capitol attack.

The current debate echoes past controversies, most notably “Operation Choke Point” during the Obama administration. Conservatives then accused the government of pressuring banks to cease services to businesses deemed high-risk, such as gun stores and payday lenders. Critics argued this was an infringement on legitimate businesses.

“Reputational Risk” Under Scrutiny

The term “reputational risk” has become a flashpoint in the debanking discussion. Banks often use it to justify decisions to end relationships with clients whose activities or associations might damage the institution’s public image or attract regulatory scrutiny. However, critics argue this amorphous concept can be weaponized to silence or exclude individuals based on their political views.

During Trump’s time in office, his administration and banking regulators took steps to curb banks’ ability to use “reputational risk” as a blanket reason for denying services. This proactive measure highlights a broader effort to prevent perceived political bias from influencing access to essential banking infrastructure. The JPMorgan case is a significant test of these regulatory intentions.

Legal Maneuvers and Broader Implications

JPMorgan is actively seeking to transfer the lawsuit from Florida state court, where Trump filed it, to federal court. Furthermore, the bank wants the jurisdiction moved to New York. Their argument is that the accounts in question were primarily located in New York, which was also the hub of many of Trump’s business operations until recently. This jurisdictional battle reflects the strategic importance of the legal venue in such a high-profile case.

This isn’t Trump’s first encounter with alleged debanking. In March 2025, The Trump Organization filed a similar lawsuit against credit card giant Capital One. That case also alleged “unjustified” account terminations and cited “woke” motivations behind the bank’s actions. The Capital One lawsuit remains ongoing, indicating a pattern of legal challenges by Trump against financial institutions.

JPMorgan’s Defense and Policy

JPMorgan has consistently maintained that Trump’s lawsuit lacks merit, even while expressing regret that he felt the need to sue. The bank’s standard account agreements typically allow either party to terminate accounts with sufficient written notice, often 30 days, with or without cause. These agreements also permit closures for specific reasons such as breach of contract, financial impairment, or violations of legal and regulatory requirements.

Bank policies emphasize regulatory compliance and risk management, covering areas like anti-money laundering, anti-terrorism, and adherence to government sanctions. Jamie Dimon, CEO of JPMorgan, publicly stated in February 2025 that his institution does not debank individuals based on political or religious affiliations. However, he acknowledged that “onerous” rules and regulatory requirements can inadvertently lead to clients being debanked. This distinction between political motives and regulatory compliance is central to the bank’s defense.

Frequently Asked Questions

What is “debanking” and why has it become so controversial?

“Debanking” refers to the practice of a financial institution closing a customer’s bank accounts or refusing to provide banking services. It has become highly controversial because figures like Donald Trump and other conservatives allege that banks are using reasons like “reputational risk” as a pretext to discriminate against individuals and businesses based on their political views. This raises concerns about freedom of speech and access to essential financial infrastructure.

Where is the Trump debanking lawsuit against JPMorgan Chase currently being litigated?

Donald Trump initially filed his $5 billion debanking lawsuit against JPMorgan Chase in Florida state court, where his primary residence is now located. However, JPMorgan Chase is actively attempting to have the case moved. The bank seeks to transfer the proceedings to federal court and to change the legal jurisdiction to New York, arguing that the accounts in question and much of Trump’s business operations were primarily based there.

How do banks typically justify closing customer accounts, and what are the implications for consumers?

Banks typically justify closing accounts based on their standard account agreements, which often allow termination with sufficient written notice (e.g., 30 days) either “with or without cause.” Specific reasons can include breach of contract, financial impairment, legal or regulatory requirements (like anti-money laundering), or activities that the bank, “in good faith,” believes violate its policies or pose a “reputational risk.” For consumers, this means banks generally have broad discretion, and understanding one’s account agreement is crucial. The implications are significant, as being “debanked” can severely disrupt personal and business finances, potentially making it difficult to open accounts elsewhere.

The admission by JPMorgan Chase marks a significant moment in the ongoing legal battle with Donald Trump. This case transcends a simple financial dispute; it delves into fundamental questions about corporate power, political influence in banking, and the rights of individuals to access financial services regardless of their political standing. As the lawsuit progresses through potential jurisdictional changes and further legal arguments, it promises to reshape the discourse around “debanking” and the responsibilities of financial institutions in a politically polarized landscape. The outcome could set important precedents for how banks manage client relationships and navigate reputational challenges in the future.